A routing number is a 9-digit code that identifies your bank in the US payment system — like your bank's address. Find it on the bottom-left of a check (the first set of numbers), or in your bank's app, website, or statement. It's also called an ABA number. Your account number (the middle set on a check) identifies your specific account; you need both for direct deposit, ACH, and wires. Big banks may have different routing numbers by state and a separate one for wires — so get yours from your own bank, not a generic search.

What a Routing Number Is

A routing number is a nine-digit code that identifies a specific bank or credit union within the US banking system. Picture it as your bank's address in the payment network: when money moves between accounts, the routing number tells the system which institution to send it to — or pull it from. Within that bank, your account number then directs the money to your exact account.

You'll see it called a few different names — ABA routing number, ABA number, or routing transit number — but they all mean the same nine-digit code. The American Bankers Association created the system back in 1910 to speed up paper check processing, and today routing numbers power direct deposit, ACH transfers, wire transfers, and check clearing alike.

A couple of fun details: A routing number is always exactly nine digits, and the first two digits fall between 00 and 12 — because they identify the Federal Reserve district that processes the bank's transactions. Also, everyone at the same bank (in the same state) usually shares the same routing number, since it identifies the institution, not you. Your account number is what makes your account unique.

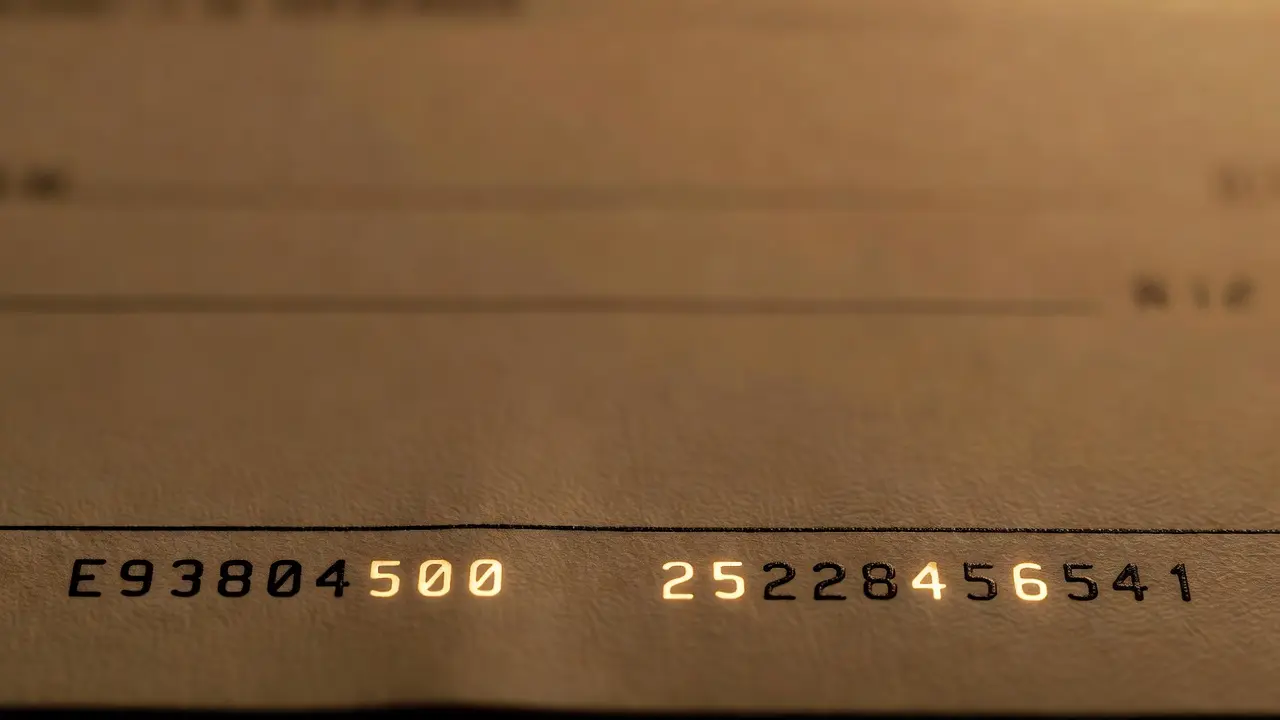

How to Read the Numbers on a Check

The fastest place to find your routing number is a paper check. The numbers along the bottom always appear in the same order — routing, account, check:

So on a check: the routing number is first (bottom-left), framed by two little symbols; the account number is second (middle); and the check number is last (bottom-right, matching the number in the top corner). This order mirrors how a payment is processed — first to the right bank, then to the right account.

Routing Number vs Account Number

Routing number

- Identifies your bank

- Always 9 digits

- Shared by all customers at your bank/state

- Public info (on every check)

- First set on the bottom-left of a check

Account number

- Identifies your specific account

- Usually 8–12 digits (varies)

- Unique to you

- Keep it private

- Second set, in the middle of a check

Both are required together for most electronic payments: the routing number handles step one (getting money to the right bank), and the account number handles step two (getting it into your account). Get either wrong and the payment can be delayed or misdirected — so double-check every digit before submitting a form.

Where to Find Your Routing Number

On a check

The first 9-digit number in the bottom-left corner, between the two symbols.

In your bank's app

Often under "Account Details" or a transfers/wires section. The most reliable source.

Bank website / FAQ

Most banks list their routing numbers online, sometimes by state.

Statement or phone

On monthly statements, or by calling your bank or visiting a branch.

Big banks have multiple routing numbers. Chase, Bank of America, Wells Fargo and others often use different routing numbers depending on the state where you opened your account — and sometimes a separate number for wire transfers. That's why you should always get your routing number from your own bank app or statement, not a generic number pulled from an internet search. Using the wrong one can delay or reject your transfer.

ACH vs Wire Routing Numbers

Some banks use different routing numbers depending on how the money moves. If your bank lists more than one, check which you need before sending:

| Type | Used for | Speed |

|---|---|---|

| ACH routing number | Direct deposit, online bill pay, most everyday transfers | 1–3 business days |

| Wire routing number | Outgoing domestic wire transfers | Usually same day |

Because wires move faster and are often used for larger amounts, using the wrong number is more costly on a wire than on an ACH transfer — so it's worth confirming with your bank which routing number to use. When you're receiving a wire, always ask your bank which routing number the sender should use. (ACH is the workhorse behind payroll, bill pay, and tax refunds; wires are for when money needs to arrive today.)

Going international? Routing numbers are US-only. For transfers to or from other countries, you'll need a SWIFT/BIC code (which identifies the bank globally) and often an IBAN (used across Europe and the Middle East). Always confirm with the receiving bank whether they need a SWIFT code, IBAN, or both.

Is It Safe to Share Your Routing Number?

Your routing number alone is public — it's on every check and shared by countless customers, so by itself it can't be used to access your account. The caution is about your account number. Routing plus account number together can set up deposits and payments, which is exactly why you give them to a trusted employer or biller — but the same combination in the wrong hands can enable fraudulent ACH debits.

Safe-sharing checklist: Only share both numbers when necessary, and only with parties you've independently verified. Never send account details by email or text — use secure channels. Monitor your account and set up alerts to catch anything unexpected, and if you suspect misuse, contact your bank immediately. In short: routing number alone is low-risk; treat the routing-plus-account combination with care. For more on protecting a shared account, see our guide on avoiding overdraft fees and opening an account online.

Frequently Asked Questions

What is a routing number?

A nine-digit code that identifies a specific bank or credit union in the US banking system — like your bank's address in the payment network. It tells the system which institution to send money to or pull it from. It's also called an ABA routing number, ABA number, or routing transit number. The American Bankers Association created it in 1910 for check processing; today it's used for direct deposit, ACH, wires, and check clearing. It's always nine digits, and the first two (00–12) identify the Federal Reserve district. Everyone at the same bank and state usually shares it. Routing numbers are US-only — international transfers use SWIFT/BIC codes and IBANs.

Where do I find my routing number?

Fastest is a paper check: it's the first nine-digit number in the bottom-left, framed by two symbols. On a check the order is routing (bottom-left), account (middle), check number (bottom-right). No checks? Find it in your bank's mobile app (often under Account Details or transfers/wires), on the bank's website or FAQ, on a statement, or by calling or visiting a branch. Caution: big banks like Chase, Bank of America, and Wells Fargo often have different routing numbers by state and sometimes a separate one for wires — so get yours from your own bank app or statement, not a generic internet search, to use the right one.

What is the difference between a routing number and an account number?

A routing number identifies your bank; an account number identifies your specific account there. The routing number is the bank's address in the payment system; the account number is your address within that bank. Routing numbers are always nine digits and shared by all customers at the same bank/state; account numbers vary (typically 8–12 digits) and are unique to you. On a check, the routing number is first (bottom-left) and the account number second (middle). Both are required together for direct deposit, ACH, and wires — routing gets money to the right bank, account gets it into the right account. Getting either wrong can delay or misdirect payment.

Is it safe to share my routing number?

Your routing number alone is public and safe — it's on every check and shared by many customers, so by itself it can't access your account. The caution is your account number. Together, routing and account numbers can set up deposits and payments, which is normal for a trusted employer or biller — but sharing both with strangers or unverified parties can enable fraudulent ACH debits. Best practices: only share both when necessary and with verified parties, never by email or text, monitor your account, and set alerts. If you suspect misuse, contact your bank immediately. Routing alone is low-risk; treat routing plus account with care.

Sources & References

- American Bankers Association — ABA Routing Number: bottom-left of check, routing then account then check, ~22,000 active 9-digit numbers

- Wells Fargo — Routing and Account Numbers Guide (March 2026): first digits = Federal Reserve district, separate ACH/wire/check numbers

- Chase — ABA vs ACH Routing Numbers: ABA from 1910, ACH from 1970s, first two digits 00–12, ACH batched same/next day

- U.S. Bank — ABA Routing Number (May 2026): 9-digit code, where to find on check/app/statement, account number in middle

- Firstcard — ABA vs Routing Number (April 2026): same 9-digit code, ACH vs wire routing, routing alone is public, SWIFT/IBAN for international

- Aspire — Routing vs Account Number (April 2026): 8–12 digit accounts, order on check, multiple routing numbers by state/type