A good credit score is 670 or higher on the FICO scale (300–850). The national average FICO score is 714 as of March 2026 — squarely in the Good tier. However, lenders typically offer their best rates to borrowers at 740 or higher (Very Good). The difference between Good (670–739) and Very Good (740+) on a 30-year mortgage can mean $40,000–$87,000 in additional interest paid over the life of the loan.

What Is a Good Credit Score — The Official FICO Ranges in 2026

FICO scores — used in 90% of U.S. lending decisions — range from 300 to 850. The scale is divided into five tiers, each corresponding to different lending terms, approval odds, and interest rates. Here's where each tier stands and what percentage of Americans fall into each category, based on 2025–2026 FICO and Experian data.

What Your Credit Score Range Actually Costs You — in Real Dollars

The abstract concept of "good credit" becomes concrete when you translate score ranges into actual dollar costs. Here's what a 30-year fixed mortgage on a $350,000 home looks like at different score ranges, based on Q1 2026 rate data from Experian and Curinos:

$350,000 Mortgage — 30-Year Fixed — Q1 2026 Rate Data

The difference between a 620 credit score and a 760 credit score on this mortgage: $356/month, or $128,160 over 30 years. That's more than a third of the original loan amount paid purely in additional interest — money that goes entirely to the lender, not toward your home equity.

Auto loans show the same pattern but compressed into a shorter timeline. On a $35,000 car loan over 60 months: a borrower with a score above 760 pays approximately $480/month at 5–6% APR. A borrower with a score below 580 pays $750–$800/month at 18–21% APR — $7,500–$15,000 more over 5 years on the exact same vehicle.

How Your FICO Score Is Calculated — the 5 Factors

FICO scores are built from five weighted factors. Understanding each one tells you exactly where to focus your improvement efforts.

The remaining 10% is new credit — hard inquiries from recent credit applications. Each hard inquiry temporarily lowers your score by 5–10 points and stays on your report for two years. Rate shopping for mortgages and auto loans within a 14–45 day window counts as a single inquiry under FICO models.

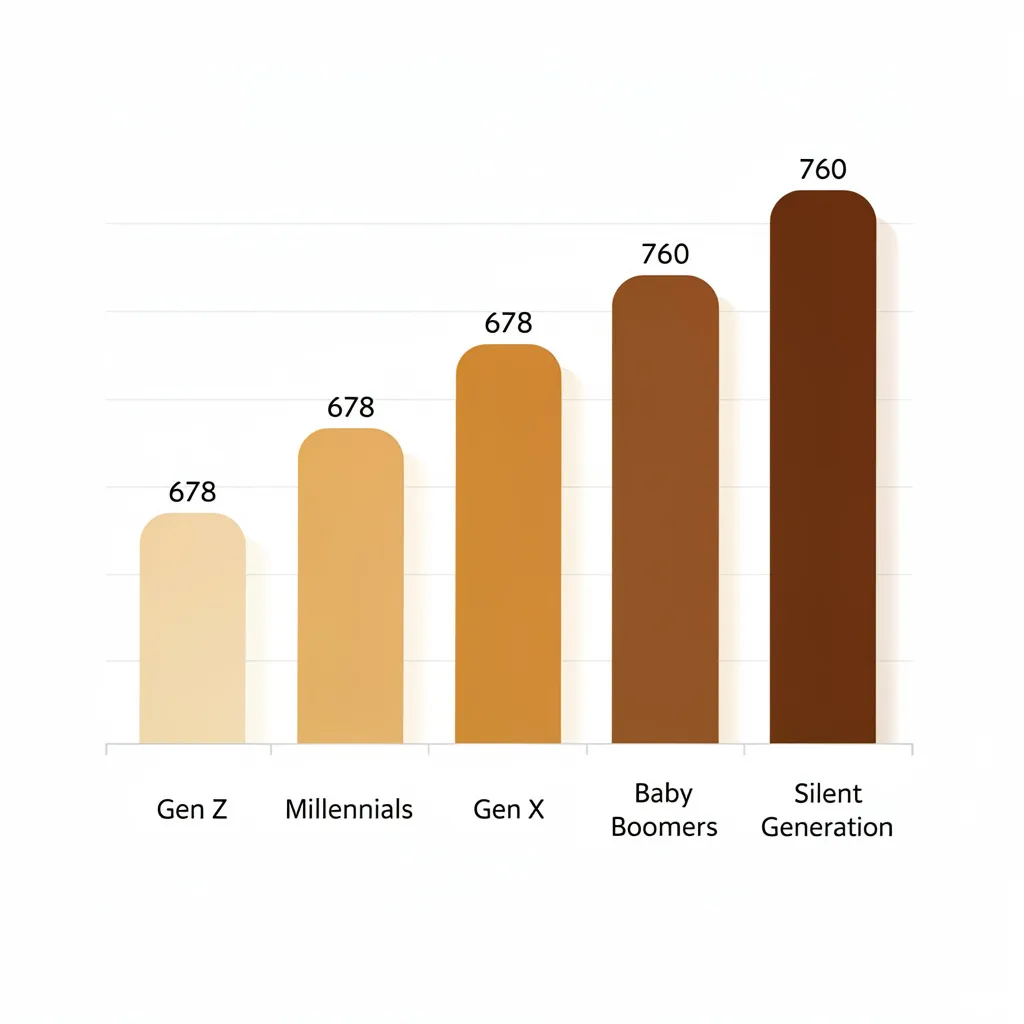

The Average Credit Score in 2026 — by Generation and State

The national average FICO score of 714 masks significant variation by age and geography. Understanding where you stand relative to your peers can provide useful context — though your score should ultimately be benchmarked against the lenders you want to access, not just your generation average.

| Generation | Age range | Average FICO (2025) | Trend |

|---|---|---|---|

| Gen Z | 18–28 | 678 | ▼ Down 3 points — student loan impact |

| Millennials | 29–44 | 689 | ▼ Down 2 points |

| Gen X | 45–60 | 709 | → Stable |

| Baby Boomers | 61–79 | 747 | ▲ Up 1 point |

| Silent Generation | 80+ | 760 | → Stable |

| National average | All ages | 714 | ▼ Down 2 points from 2024 peak |

The generational pattern reflects credit history length more than financial discipline. Gen Z's lower average is largely mathematical — they've had less time to build history. Baby Boomers and the Silent Generation benefit from decades of established credit relationships.

Geographically, the highest state averages are in the Northeast and West (Minnesota leads at 725), while the lowest are in the South (Mississippi at 670). The spread is 55 points between the highest and lowest state averages.

What Credit Score Do You Need for Major Financial Products in 2026?

| Financial product | Minimum score | Best rates score | Notes |

|---|---|---|---|

| Conventional mortgage | 620 | 760+ | $87K+ difference in total interest over 30 years |

| FHA mortgage | 500 (10% down) or 580 (3.5% down) | N/A | Government-backed — more accessible |

| Auto loan (new car) | 580–620 | 740+ | Sub-600 pays 18–21% APR vs 5–6% for 760+ |

| Balance transfer card (0% APR) | 670 | 720+ | Good credit required for best intro periods |

| Personal loan (best rates) | 580 | 720+ | 720+ typically qualifies for sub-12% APR |

| Premium travel credit card | 700 | 750+ | Best rewards cards require strong credit |

| Apartment rental | 620–650 (most landlords) | 720+ | Varies significantly by landlord and market |

How to Improve Your Credit Score — Fastest Methods in 2026

If your score is below where you want it, here's where to focus, ordered by speed of impact:

- Dispute errors on your credit report. Pull free reports from AnnualCreditReport.com. The FTC found 1 in 5 Americans has a verified error. CFPB research shows successfully resolved disputes average a 25-point improvement — some exceed 100 points when major errors are removed. This is the fastest possible win if errors exist.

- Reduce credit utilization below 10%. Pay down credit card balances before your statement closes (not just by the due date). This impacts 30% of your score and shows results within one billing cycle.

- Use Experian Boost. Add utility, phone, and streaming payment history to your Experian score instantly. No cost, can add points within minutes.

- Become an authorized user. Being added to a family member's or partner's credit card with a long, clean history can add significant positive history to your report within 30–60 days.

- Never miss a payment — set up autopay. One 30-day late payment can drop a 780 score by 60–100 points and stays on your report for 7 years. Autopay for minimum payments is non-negotiable.

For the complete guide to raising your credit score by 100 points, see: How to Raise Your Credit Score 100 Points — Strategies Ranked by Real Impact.

2026 scoring update: FICO 10T — now required for mortgage underwriting alongside older models — incorporates 24 months of credit behavior trends. Consistent improvement over time is increasingly recognized and rewarded. This means someone who steadily reduced utilization over 18 months benefits more under FICO 10T than under FICO 8, which only looks at a current snapshot.

Frequently Asked Questions

What is considered a good credit score?

A good credit score is 670 or higher on the FICO scale (300–850). FICO's tiers: 300–579 Poor, 580–669 Fair, 670–739 Good, 740–799 Very Good, 800–850 Exceptional. The national average is 714 as of March 2026 — Good tier. However, lenders offer their best rates to borrowers with 740 or higher.

What credit score do you need to buy a house in 2026?

For a conventional mortgage, most lenders require 620 minimum. Best rates go to 760+. FHA loans are available from 500 (10% down) or 580 (3.5% down). The difference between 620 and 760 on a $350,000 30-year mortgage is roughly $128,000 in total interest based on Q1 2026 rates.

How long does it take to build a good credit score?

From zero history: a basic score generates within 3–6 months. Reaching 670+ (Good) typically takes 12–24 months of consistent on-time payments and low utilization. The 740+ (Very Good) tier generally requires 2–4 years of positive history. Fastest path: secured credit card plus Experian Boost, never miss a payment, keep utilization below 10%.

What is the average credit score in the US in 2026?

The average FICO Score is 714 as of March 2026, according to FICO's Credit Insights Report. Down from the 717 peak in 2023, driven by rising credit card utilization and resumed student loan delinquency reporting. The average VantageScore 3.0 is 698. Despite the slight decline, 70% of Americans have a score of 670 or higher.

Does checking your credit score lower it?

No. Checking your own credit score is a soft inquiry with zero impact. You can check it as often as you like for free through Experian, Credit Karma, or your bank's credit tool. Only hard inquiries — when a lender checks your credit for a new application — can temporarily lower your score by 5–10 points.

Sources & References

- FICO — FICO Score Credit Insights Report, Fall 2025 (national average 715; 48.1% at 750+)

- FICO — FICO Score Credit Insights, March 2026 (average FICO Score dips to 714)

- Experian — State of Credit 2025 (average FICO 713; 70% have 670+; generational breakdown)

- NerdWallet — Average Credit Score by Age, March 2026 (average FICO 714)

- Experian / Curinos — Mortgage rate data by credit score tier, Q1 2026

- Federal Housing Finance Agency — FICO 10T mortgage underwriting requirement, 2026

- CFPB — Credit report disputes: average 25-point improvement on resolved errors

- FTC — Credit report errors study: 1 in 5 Americans has verified error