The 50/30/20 rule divides your after-tax income into 50% for needs (rent, groceries, utilities, insurance, minimum debt payments), 30% for wants (dining out, entertainment, subscriptions), and 20% for savings and debt payoff. It works well as a starting framework, but in 2026 — with the average American spending 34% of income on housing alone — many people need to run 60/20/20 or 65/15/20 depending on their city. The 20% savings floor is the most important number: protect it first before allocating to wants.

What the 50/30/20 Rule Is — and Where It Came From

The 50/30/20 rule was popularized by Senator Elizabeth Warren and her daughter Amelia Warren Tyagi in their 2005 book All Your Worth: The Ultimate Lifetime Money Plan. The framework is simple: divide your monthly after-tax income into three categories and allocate a target percentage to each.

The rule uses after-tax income — your actual take-home pay — not your gross salary. This is the most common mistake people make when applying it. Using your $80,000 gross salary instead of your $61,000 after-tax take-home inflates every category by about 31% and makes the math feel more generous than it actually is.

Your 401(k) contributions that come out automatically before you receive your paycheck can count toward the 20% savings allocation — effectively increasing your apparent take-home for budgeting purposes while the savings still happen.

The 50/30/20 Rule in Practice — Real Examples by Income

These numbers look achievable in the abstract. In practice, anyone living in a high-cost city quickly discovers that the 50% needs allocation disappears on rent alone. The Federal Reserve Bank of St. Louis noted that the rent-to-income ratio has been structurally above 30% for over a decade — meaning the "needs" category is already at 30% before adding groceries, insurance, utilities, or transportation.

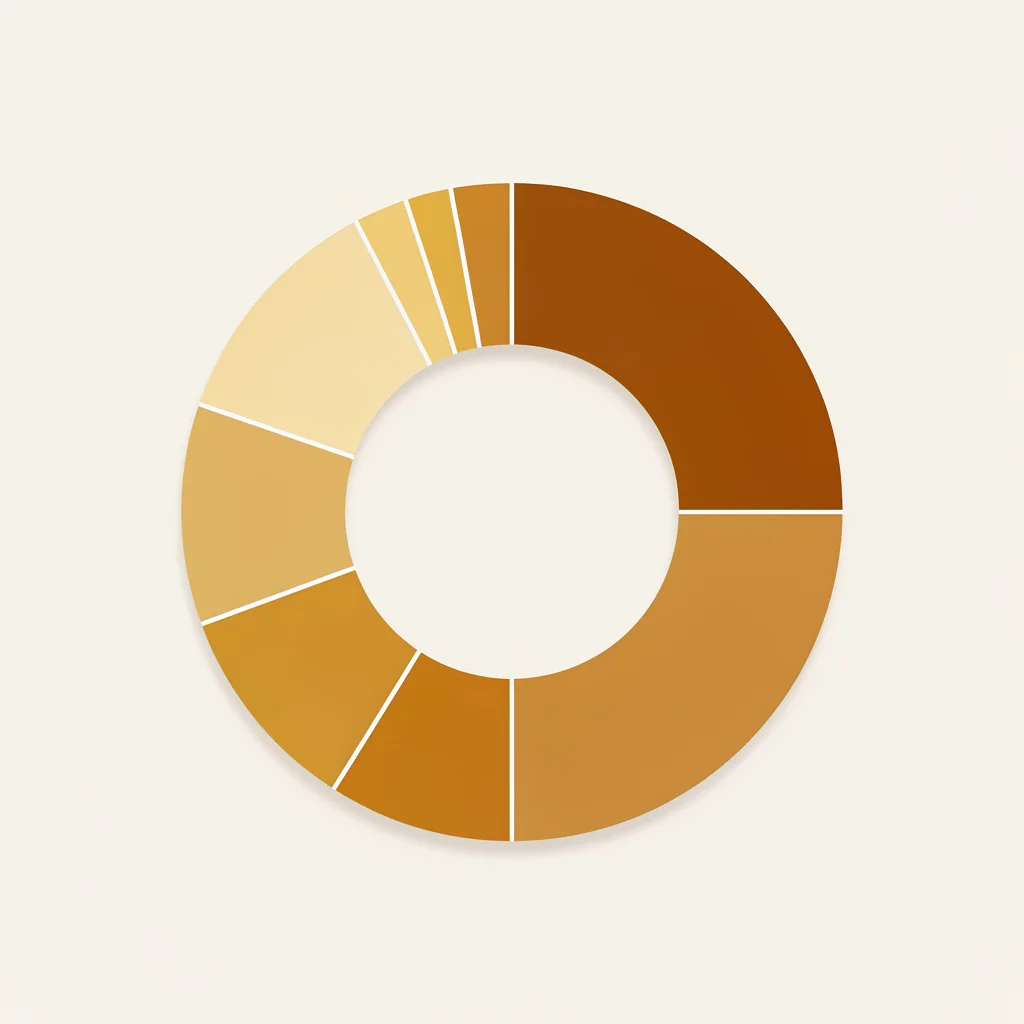

How Americans Actually Split Their Paychecks in 2026

The gap between the ideal 50/30/20 and reality is stark. A Talker Research and EarnIn survey of Americans earning $75,000 or less found the actual average split is dramatically different from the rule's target:

The average American is spending 14 percentage points more on needs than the rule targets — and sacrificing both wants and savings to cover it. Housing is the primary driver: in 2026, the average American spends 34% of income on housing alone, according to BLS Consumer Expenditure Survey data. That leaves only 16% of the needs budget for everything else — groceries, utilities, transportation, insurance, and minimum debt payments.

This doesn't mean the rule is broken. It means the baseline reality is harder than the rule's authors anticipated in 2005. The practical question isn't whether you can hit the ideal percentages — it's how to use the framework to make the best allocation decisions given your actual income and geography.

What Counts as a Need vs. a Want — The Distinctions That Matter

The most important and most contested part of the 50/30/20 rule is the line between needs and wants. Getting this wrong inflates the needs category and makes the rule feel unworkable even when it isn't.

True needs — expenses you cannot cut without significantly disrupting your life:

- Housing: rent or mortgage payment (at a reasonable level for your city)

- Basic utilities: electricity, water, heat, internet for work

- Groceries: food at home, basic cooking supplies

- Transportation to work: car payment, gas, insurance — or public transit

- Health insurance and essential medications

- Minimum required debt payments: credit card minimums, loan minimums

- Basic clothing and personal hygiene items

Wants disguised as needs — expenses that feel necessary but aren't:

- Housing more expensive than a functional alternative in your area

- A newer or more expensive car than required to get to work reliably

- Restaurant meals and takeout (groceries are a need — dining out is a want)

- Gym memberships, streaming subscriptions, premium phone plans

- Brand-name clothing when basics would suffice

- Travel and vacations

The most common misclassification: Housing. A $2,500/month apartment in a city where $1,400/month apartments exist and serve the same function — the extra $1,100/month is a want, not a need. This doesn't mean you shouldn't live there — it means that choice affects your 30% wants allocation, not your 50% needs allocation. Recognizing this gives you more control over the outcome.

When the 50/30/20 Rule Needs to Be Adapted

The rule is a starting point, not a law. Three situations consistently require adaptation:

High-cost cities

If you live in San Francisco, New York, Los Angeles, Boston, or Seattle, housing alone may consume 40–50% of your take-home pay at reasonable market rates. Running 60% or 65% on needs isn't a failure — it's arithmetic. In this case, compress the wants category to 15–20% and protect the savings floor at 20%. A 60/20/20 or 65/15/20 split is functionally sound even if it doesn't match the textbook rule.

High debt loads

If you're carrying significant high-interest debt — credit cards, personal loans above 7% — aggressively redirect from the 30% wants bucket to debt payoff. The extra debt payments count toward the 20% savings/debt category. A person with $15,000 in credit card debt at 21% APR should be running something closer to 50/10/40 until the debt is eliminated — then restoring the wants allocation.

Low income

At very low income levels, the 50% needs allocation may not be achievable because needs genuinely consume 70–80% of income regardless of lifestyle choices. In this situation, the rule functions differently: focus on reducing needs costs wherever possible (food waste, lower-cost housing, eliminating all non-essential costs), build even a small savings habit ($25–$50/month automated), and prioritize income growth as the primary goal.

The One Number to Protect Above Everything Else

If you can only get one piece of the 50/30/20 rule right, protect the 20% savings allocation. This is the number that determines your financial trajectory more than any other.

The 50% needs bucket can flex between 45% and 65% depending on your city and life stage without long-term damage. The 30% wants bucket can compress to 10–15% when you're in debt payoff mode and expand to 35% when you're debt-free and earning more. But consistently saving 20% of your income — through good months and difficult ones — is what builds the emergency fund, the retirement account, and eventually the financial freedom that makes the whole thing worthwhile.

Research from The Penny Hoarder found that 48% of Americans only save whatever is left after bills are paid. "Whatever is left" is rarely 20% — and usually zero. The structural solution is automation: set up an automatic transfer on payday for your savings target before anything else gets spent. The 50/30/20 rule works best not as a tracking exercise but as a directive for where to point your automated transfers.

Alternatives When 50/30/20 Doesn't Fit

How to Start the 50/30/20 Rule — A Practical Setup

- Calculate your actual monthly take-home pay. Check your bank deposits or last pay stub. Use the net amount — after taxes, health insurance, and any 401(k) deductions that come out automatically.

- List every expense from the last 2–3 months. Pull bank and credit card statements. Categorize each item as need, want, or savings. Be honest about which category an expense truly belongs to.

- Calculate your current percentages. Add up each category and divide by take-home pay. Compare to 50/30/20. This diagnostic step shows exactly where the pressure is.

- Set up automatic transfers on payday. Before anything else moves, transfer your savings target to a high-yield savings account. This is the most important structural change.

- Adjust percentages to your reality. If needs genuinely require 60%, run 60/20/20 and work toward reducing needs costs over time. Don't set an unachievable target that causes you to abandon the system in week two.

- Review monthly for the first 3 months. Look at actual spending against targets. The first month is always instructive — you'll find categories you forgot and items you misclassified.

The most common failure mode: Setting a perfect 50/30/20 target that's completely disconnected from current spending, failing to hit it in month one, and abandoning the entire system. An imperfect budget you follow consistently beats a perfect budget you follow for two weeks. Start with your real numbers, adjust slightly, and iterate from there.

Frequently Asked Questions

What is the 50/30/20 rule?

The 50/30/20 rule divides your monthly after-tax income into three categories: 50% for needs (rent, utilities, groceries, insurance, minimum debt payments), 30% for wants (dining out, entertainment, subscriptions), and 20% for savings and extra debt payments. Popularized by Elizabeth Warren's 2005 book. Always uses after-tax income — your actual take-home pay, not gross salary.

Does the 50/30/20 rule work in 2026?

It works as a framework, but the exact percentages are difficult to hit for many Americans. The average American spends 34% of income on housing alone in 2026. Survey data shows Americans earning $75,000 or less actually spend 64% on needs, 16% on wants, and 16% on savings. Most practical approach: use 50/30/20 as a diagnostic tool and adapt percentages to your situation while protecting the 20% savings floor above all else.

What counts as a 'need' vs a 'want' in the 50/30/20 rule?

Needs: housing, basic utilities, groceries, work transportation, health insurance, minimum debt payments. Wants: dining out, entertainment, streaming subscriptions, vacations, premium housing or cars beyond functional needs. Most common misclassification: housing and transportation. A $3,000/month apartment when a $1,500 apartment would suffice — the extra $1,500 is a want, not a need.

What if my needs take up more than 50% of my income?

Adjust the percentages proportionally while protecting your savings rate. If needs genuinely consume 60–65% of income, reduce wants to 15–20% and maintain a 20% savings floor. If you can't reach 15% savings after covering true needs, that signals your income needs to grow or you need to reduce fixed costs. A 60/20/20 or 65/15/20 split is functionally sound even if it doesn't match the textbook rule.

Should I use gross or net income for the 50/30/20 rule?

Always use net income — your actual take-home pay after taxes and mandatory deductions. Using gross salary inflates every budget category significantly. Your 401(k) contributions that come out automatically can be counted as part of the 20% savings allocation, effectively increasing your apparent take-home for budgeting purposes while the savings still happen.

Sources & References

- Talker Research / EarnIn — Survey of Americans earning $75,000 or less: actual spend breakdown 64% needs, 16% wants, 16% savings (GOBankingRates, 2026)

- Bureau of Labor Statistics — Consumer Expenditure Survey 2024: housing = 33% of total annual spending; average household $504/month food at home

- Federal Reserve Bank of St. Louis — rent-to-income ratio structurally above 30% for over a decade

- National Low Income Housing Coalition — 2024 report: average renter needs to earn over $90,000 to afford a two-bedroom apartment

- The Penny Hoarder — State of Savings survey: 48% of Americans save only what's left after bills; 65% say essential living costs are their biggest source of financial anxiety

- Wealthvieu — 50/30/20 Rule 2026: average American spends 34% on housing alone (May 2026)

- Elizabeth Warren & Amelia Warren Tyagi — All Your Worth: The Ultimate Lifetime Money Plan, 2005 (origin of the 50/30/20 rule)